Our Q2 benchmarking report, based on 1,761 single origin coffees from 250 roasters, tracks how coffees are priced, which certifications are used, what origins are trending, and more.

Below we outline the top 3 surprising results from our analysis:

Organic Coffees Are Selling at a Discount – Not a Premium

For years, the Organic certification has been framed as a signal of higher quality, stronger environmental practices, and added value for conscious consumers. One would expect that to translate into higher retail prices for roasted coffee.

But across our Q2 dataset, the opposite trend emerged.

On average, certified Organic coffees were priced $0.40 less per ounce than their non-organic counterparts – controlling for origin.

This pattern held across Latin American, African, and Asian origins, with some regional variation but the same overall direction: Organic coffee was being sold at lower prices. The sample included both single-certification (Organic only) and dual-certified (Organic + Fair Trade) coffees, but even the combined group underperformed in price relative to uncertified coffees of the same origin.

This counters the typical narrative that Organic coffees deserve or receive a price premium. Instead, it suggests that Organic labeling – at least among the roasters in our sample – is not being used, or is not able, to signal exclusivity or command higher retail margins. Whether this is due to pricing pressure, consumer skepticism, or other market forces is beyond the scope of this dataset, but the discount is real and statistically significant.

Most Coffees in the Marketplace Carry No Certification at All

A second trend that stood out this quarter was just how rare certifications are across the specialty coffee landscape.

Out of the 1,761 single origins we analyzed:

- 1,398 had no certifications at all

- 122 were labeled Organic only

- 149 were dual-labeled Organic + Fair Trade

Other combinations with other certifications (such as Rainforest Alliance or Smithsonian Bird Friendly) exist, but in very small numbers. That means nearly 80% of coffees in our sample were uncertified. In a sector where storytelling, transparency, and values-based marketing are central themes, this is a counterintuitive finding.

Put another way: Certified coffees (Organic, Fair Trade, or other) made up just 20% of all offerings.

Despite the growth of ethical sourcing conversations in trade shows, newsletters, and branding efforts, certifications appear to play a relatively minor role in the actual retail offerings of small, specialty roasters.

This finding aligns with a growing body of research suggesting that roasters may be moving away from third-party certifications in favor of direct-trade relationships, farming techniques that are modeled after Organic standards but not technically certified as such, or origin-focused storytelling emphasizing values over certifications. The departure from pursuing certifications may also be because their importance has been watered down by claims of fraud or insufficient monitoring. This is most notably the case with the Organic certification process.

However, certifications still serve as a third-party standard that can gain consumer trust, especially as consumers typically have no other way of independently verifying certifications. But their limited retail presence raises questions about how sustainability is being signaled – and who is expected to care.

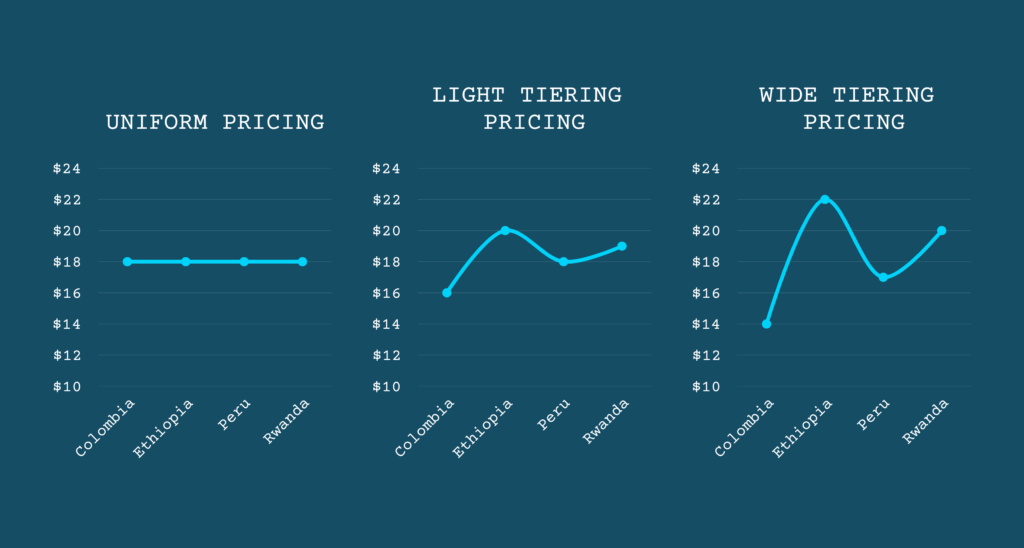

Roasters with “Wide Tiering” Price Models Capture Higher Premiums

The third key finding relates to pricing strategy – and here, there’s some good news for roasters willing to differentiate their offerings more sharply.

Roasters who used a “wide tiering” model – meaning they price different coffees at clearly different levels based on origin – captured a $0.25 per ounce premium over the median per-origin price.

This approach stood in contrast to “uniform pricing,” where most or all coffees (regardless of origin) are priced identically, and to “light tiering”, where prices vary more tightly.

Only 84 of the 250 roasters in the sample used wide tiering. But those who did saw a clear pricing benefit.